Debt Fire? How I Stayed Calm and Protected My Future

You’re not alone if you’ve ever felt trapped by debt—like one missed payment could collapse everything. I’ve been there, heart racing as bills piled up. But panic doesn’t fix anything. What saved me wasn’t luck; it was learning how to act fast, think clearly, and avoid deadly financial mistakes. This is how I navigated the storm—and how you can too, without losing sleep or hope. Financial stress doesn’t discriminate. It can hit anyone, even those who’ve lived carefully, saved when possible, and planned for the future. A medical emergency, a sudden job loss, or an unexpected home repair can shift stability into uncertainty in days. The real danger isn’t just the debt itself—it’s how we respond when overwhelmed. Many people, in their effort to survive the moment, unknowingly set themselves up for longer-term damage. This story isn’t about magic fixes or overnight success. It’s about clarity, control, and the practical steps that truly protect your future.

The Moment Everything Felt Like It Was Breaking

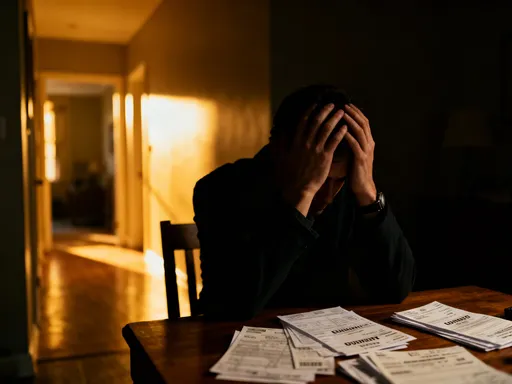

It started quietly, as these things often do. A car repair here, a doctor’s visit there—each expense manageable on its own, but together they began to pile up. At first, I told myself it was temporary. I had a stable job, a modest savings account, and a history of paying bills on time. But when a family emergency required travel and time off work, the cracks began to show. Income dipped. Expenses rose. And then came the notice from the credit card company: a higher minimum payment due to increased interest. That’s when the fear set in—not just concern, but a deep, physical dread. My chest tightened every time the phone rang, worried it was a collector. I stopped opening mail. I avoided checking my bank balance. The numbers felt like they were spinning beyond my control, and I felt powerless to stop them.

This emotional spiral is more common than most people admit. Financial shame often keeps these struggles hidden, even from close friends and family. But the truth is, debt distress isn’t a moral failing—it’s a human response to pressure. When overwhelmed, the brain shifts into survival mode. Rational thinking dims. Decisions become reactive rather than strategic. Some people turn to more credit, hoping to bridge the gap. Others hide from the problem entirely, hoping it will resolve itself. Neither approach works. In fact, both can deepen the crisis. What I eventually realized was that the real emergency wasn’t just the debt—it was the loss of perspective. The moment I accepted that I needed a plan, not a miracle, everything began to change. Admitting I was in over my head wasn’t weakness; it was the first step toward regaining control.

That turning point came on a Tuesday morning. I sat at my kitchen table, coffee cold, surrounded by unopened envelopes. Instead of shoving them aside, I opened one. Then another. I listed every debt, every due date, every interest rate. The total wasn’t surprising, but seeing it in black and white made it real. And strangely, that clarity brought relief. The unknown had been the worst part. Now, I had data. I had facts. And with those, I could start building a response—not based on fear, but on reality.

Why Most People Make Debt Crises Worse (Without Realizing It)

When under financial pressure, people often take actions that feel logical in the moment but cause long-term harm. One of the most common mistakes is avoiding communication with creditors. It’s understandable—no one wants to face the conversation about missed payments. But silence doesn’t stop interest from accruing or penalties from applying. In fact, it often triggers them. Many lenders have hardship programs, temporary forbearance options, or revised payment plans, but they can’t offer help if you don’t reach out. By staying silent, you lose access to potential solutions and risk damaging your credit score unnecessarily.

Another dangerous pattern is relying on new debt to manage old debt. Transferring balances to a card with a 0% introductory rate might seem smart, but if the balance isn’t paid off before the promotional period ends, the interest rate can skyrocket. Worse, opening new accounts increases credit inquiries and can lower your average account age, both of which may hurt your credit score. Some people take cash advances or use payday loans, not realizing how quickly the fees and interest accumulate. These short-term fixes often extend the problem, sometimes doubling or tripling the original amount owed over time.

Paying only the minimum is another trap disguised as responsibility. It feels like progress because you’re technically meeting obligations, but with high-interest debt, most of that payment goes toward interest, not the principal. A $5,000 credit card balance at 22% interest, paid at the minimum (typically 2-3% of the balance), could take over 20 years to pay off and cost more than $8,000 in total. That’s not debt relief—that’s long-term financial captivity. The issue isn’t laziness or lack of discipline; it’s a lack of awareness about how compound interest works against you when you’re not paying strategically.

Perhaps the most overlooked mistake is neglecting other financial priorities in the name of debt repayment. Some people drain their emergency fund to pay off credit cards, leaving themselves vulnerable to the next unexpected expense. Others stop contributing to retirement accounts, sacrificing future security for present relief. While the intention is noble, the outcome can be counterproductive. Financial health isn’t just about eliminating debt—it’s about maintaining balance. Eliminating one risk while creating another isn’t progress. It’s substitution. The goal should be to reduce debt without compromising your ability to handle future shocks.

Stop the Bleeding: Immediate Actions That Actually Work

When you’re in a debt crisis, the first priority isn’t to fix everything—it’s to stabilize. Think of it like an emergency room: you don’t perform surgery on day one. You stop the bleeding first. The same principle applies to finances. The goal in the first 72 hours is to regain a sense of control by taking concrete, manageable steps. The most effective starting point is to freeze all non-essential spending. That doesn’t mean living in austerity forever—it means pausing discretionary purchases like dining out, subscriptions, or retail therapy. These aren’t luxuries you’re giving up permanently; they’re temporary pauses that free up cash for more urgent needs.

Next, create a bare-bones budget. This isn’t your regular monthly budget. It’s a survival version that includes only essentials: housing, utilities, groceries, transportation, and minimum debt payments. List your income, even if it’s reduced, and match it against these core expenses. The goal is to see where you stand today—not next month, not when things improve, but now. This exercise often reveals small gaps that can be closed with minor adjustments, like switching to a cheaper phone plan or carpooling. More importantly, it helps you identify how much, if any, extra cash can be directed toward debt without sacrificing basic needs.

Then, pick up the phone and call your creditors. This step feels intimidating, but it’s one of the most powerful actions you can take. Most major lenders have hardship departments trained to help customers in temporary distress. You can request lower interest rates, deferred payments, or extended due dates. These aren’t favors—they’re tools designed to keep borrowers from defaulting. Be honest about your situation. Provide documentation if asked. Many people hesitate because they fear judgment, but customer service teams handle these calls every day. Their job is to keep accounts active, not to shame callers. By communicating early, you protect your credit, avoid late fees, and open the door to workable solutions.

Finally, consolidate your information. Create a single document—a spreadsheet or notebook page—that lists every debt: creditor name, balance, interest rate, minimum payment, and due date. Update it weekly. This becomes your financial dashboard, a clear picture of where you stand. Seeing progress, even small reductions in balances, builds confidence. More importantly, it keeps you from making decisions based on emotion. When you’re stressed, it’s easy to misremember which bill is most urgent. This document removes guesswork. It turns chaos into order. And order is the foundation of recovery.

Know Your Debt Types—Because Not All Debt Is Equal

One of the biggest mistakes people make in debt repayment is treating all debt the same. They throw extra money at whatever feels most urgent, without considering the long-term consequences. But not all debt carries the same risk. Understanding the differences between secured and unsecured debt, revolving credit and installment loans, is essential for making smart decisions. Secured debt—like a mortgage or auto loan—is backed by an asset. If you default, the lender can repossess the car or foreclose on the home. This makes it high-risk in terms of consequences, even if the interest rate is low. Unsecured debt—like credit cards or personal loans—has no collateral, so the lender can’t seize property, but they can sue or send the debt to collections, which harms your credit.

Revolving credit, such as credit cards, allows you to borrow up to a limit and pay it back over time. The danger lies in the variable interest and minimum payment structure, which can trap you in a cycle of long-term repayment. Installment loans, like student loans or auto financing, have fixed payments over a set term. They’re more predictable but can still carry high interest, especially if your credit isn’t strong. The key is to prioritize based on both interest rate and risk. High-interest unsecured debt, like credit cards at 20% or more, should generally be targeted first because it grows fastest. But if you’re at risk of losing your home or car, those secured obligations may need immediate attention, even if the rate is lower.

Another important distinction is between good debt and bad debt, though these labels can be misleading. ‘Good’ debt, like a mortgage or student loan, is expected to increase your long-term financial potential. ‘Bad’ debt, like high-interest credit card spending on non-essentials, doesn’t. But context matters. A student loan for a degree you never completed may not be ‘good,’ and a credit card used for a necessary home repair could be a responsible use of debt. The real question isn’t whether the debt is good or bad—it’s whether it’s manageable and aligned with your goals. By categorizing your debts, you can create a repayment strategy that reduces both cost and risk, rather than reacting emotionally to the largest balance or the loudest creditor.

The Risk-Aware Repayment Strategy No One Talks About

Most debt advice focuses on speed: pay it off as fast as possible. But a faster repayment plan isn’t always a smarter one. The risk-aware strategy balances urgency with sustainability. It recognizes that financial recovery isn’t a sprint—it’s a marathon. Pushing too hard, too fast, can lead to burnout or new crises. For example, if you divert every extra dollar to debt and then face an unexpected car repair, you might have to borrow again, restarting the cycle. The smarter approach is to pay down debt aggressively but not at the expense of other critical protections.

This strategy starts with protecting a small emergency fund—even $500 to $1,000. That may seem counterintuitive when you’re in debt, but it acts as a financial shock absorber. Without it, any surprise expense becomes a crisis. With it, you can handle minor emergencies without adding new debt. Next, maintain essential insurance—health, auto, renters or homeowners. Letting coverage lapse to save money is risky. A single accident or illness could result in bills far larger than any debt you’re trying to eliminate. Similarly, don’t stop retirement contributions entirely, especially if your employer offers a match. That match is free money, and pausing contributions means losing years of compound growth, which is hard to recover later.

When allocating extra payments, use a hybrid approach. Focus on high-interest debt first (the avalanche method), but consider the psychological benefit of paying off smaller balances quickly (the snowball method). Some people stay motivated by seeing accounts close, even if it’s not the most mathematically efficient. The best strategy is the one you can stick to. Automate payments to avoid missed deadlines. Set up alerts for due dates. And track progress monthly. The goal isn’t perfection—it’s consistent, thoughtful action. Over time, this balanced method reduces debt, protects your future, and builds lasting financial resilience.

Building Your Financial Shock Absorbers

Once the immediate crisis is under control, the focus must shift from survival to strength. Just as a car needs shock absorbers to handle rough roads, your finances need buffers to withstand unexpected events. The most effective protection isn’t a single action—it’s a system of small, sustainable habits that reduce vulnerability. Start with micro-savings. Even $20 a week adds up to over $1,000 in a year. Set up automatic transfers to a separate savings account so the money is out of sight and out of mind. This fund isn’t for vacations or shopping—it’s for true emergencies: a broken appliance, a medical co-pay, a sudden travel need.

Next, safeguard access to credit. If you’ve paid off a credit card, consider keeping the account open, even if you don’t use it. Closing it reduces your total available credit, which can increase your credit utilization ratio and lower your score. Instead, store the card in a safe place and use it occasionally for a small, necessary purchase—like a tank of gas—then pay it off immediately. This keeps the account active and helps maintain a longer credit history, both of which support a healthier credit profile.

Income diversification is another powerful buffer. Relying on a single source of income makes you more vulnerable to job loss or industry downturns. Look for ways to add a secondary stream, even if it’s small. This could be freelance work, a part-time gig, selling unused items, or monetizing a hobby. It doesn’t have to replace your main job—just provide enough to cover a month’s essentials if needed. Many people discover that these side efforts not only boost financial security but also increase confidence and creativity.

Finally, build a support network. Financial isolation makes problems feel larger. Talk to a trusted friend, join a community group, or consult a nonprofit credit counselor. These connections provide not just advice but emotional support. Knowing you’re not alone makes challenges easier to face. Over time, these shock absorbers transform your relationship with money. You stop living in fear of the next crisis and start building a foundation that can handle it.

Staying Safe: Habits That Keep Risk Low Long After the Crisis

Recovery isn’t a one-time event—it’s a series of ongoing choices. The habits you build after a debt crisis are what prevent relapse. One of the most powerful is spending awareness. That doesn’t mean tracking every coffee, but understanding your patterns. Review your bank statements monthly. Ask: Where did my money go? Were those expenses aligned with my values? This isn’t about guilt—it’s about insight. When you see how money flows, you can make intentional adjustments. Maybe you spend more on convenience than you realized. Or perhaps subscriptions have quietly added up. Awareness creates space for change.

Another essential habit is the routine budget check-in. Set a weekly or monthly time to review your income, expenses, and goals. Treat it like a doctor’s appointment—non-negotiable. Use this time to adjust for changes, celebrate progress, and catch small issues before they become big ones. A budget isn’t a restriction; it’s a roadmap. It shows you where you are and helps you navigate toward where you want to be.

Practice delayed gratification. When you want to make a non-essential purchase, wait 48 hours. Often, the urge passes. If it doesn’t, you can proceed with intention, knowing it’s a choice, not an impulse. This simple pause reduces emotional spending and builds financial discipline. Over time, it becomes second nature.

Finally, redefine success. Financial health isn’t about having zero debt or a perfect credit score. It’s about peace of mind. It’s knowing you can handle life’s surprises without falling apart. Progress, not perfection, is the goal. There will be setbacks. But each time you respond with clarity instead of panic, you strengthen your resilience. You’re not just recovering from a debt crisis—you’re building a future where you’re in control, protected, and prepared for whatever comes next.